via taxi-point https://ift.tt/2lRf6Jw

July 05, 2018 at 07:52AM https://ift.tt/2ufVjKI THESE POSTS ARE NOT OUR ENDORSEMENT

July 05, 2018 at 07:52AM https://ift.tt/2ufVjKI THESE POSTS ARE NOT OUR ENDORSEMENT

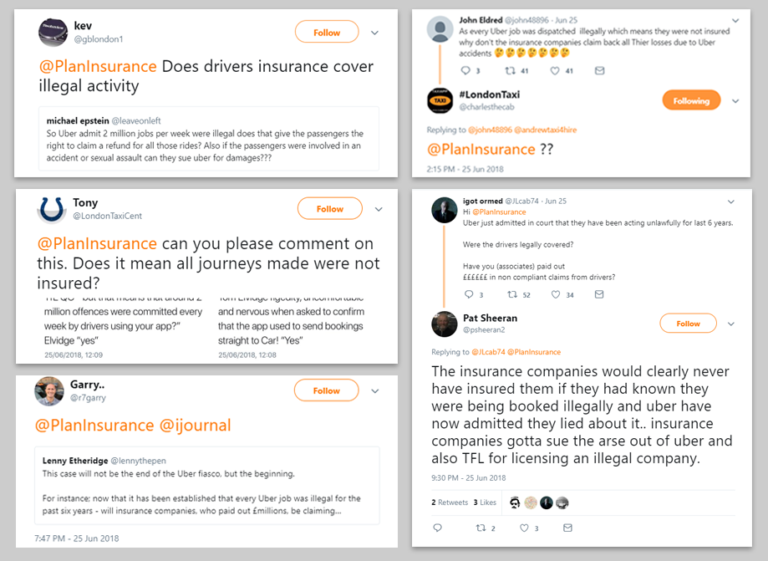

Following the recent hearing and Uber’s admission that they’ve been circumnavigating TfL’s licensing requirements for the past 6 years, we received a lot of queries on social media about whether insurers should pursue Uber for claims payouts during this period. Also, questions have been asked to whether their drivers should have their insurance policies cancelled/voided.It’s important to point out that we aren’t an insurer, and as a broker, we have no vested interest in them doing so or not, but we’ve tried to anticipate what the outcome would be of an insurer pursuing that course of action, in response to the queries we have received.

Can an insurer void a policy?

Due to Article 75, an insurer has the right to void a policy and cease proceedings on the policyholders claim. However, they are still obliged to pay the third party. So, since Uber has been trading for over 5 years now, an insurer would have to go through all its historical claims and contact each person to find out if, at the time of the incident, they were transporting an Uber passenger.This process would take a very long time and cost a lot of money to the insurer! If they did successfully find a driver that matched the criteria, they would then have to take the driver to court. The issue here is that, unless the driver has sufficient income to be in a position to pay, it would be very unlikely that the insurer would get any of its money back. This could, therefore, be a very lengthy and costly process, just to void someone’s policy.So, in theory, they could try and do it; but they would still have to pay the third party cost and then try to retrieve the money back. This would be virtually impossible, as it would cost the insurer much more on top of what they have already paid!Complaining to the Financial Ombudsman (FOS)

Now, if an insurer was to go through the process, and the policyholder was to complain to the FOS, it would look at it and rule in the policyholder’s favour, on the following grounds:

The customer bought the policy in good faith – They were told by TFL they needed XYZ (a Medical, a Vehicle which is licensed, a DBS Check etc.) and insurance which covers their vehicle for Private Hire. They also had no reason to believe that they could not work for Uber; as TFL never said they could not.Also, they would more than likely class the policyholder as a vulnerable customer, particularly if they are on a low income, and English is their second language. The FOS are likely to view it as a “big corporate insurer” trying to squash a “little private hire driver”; and take this into consideration on their decision. You can read more regarding vulnerable customers on the FOS and the FCA’s websites.Lastly, the FOS would also ask:If the driver was an operator would you have still insured them? And the insurer would most likely say YesHad you known he worked for Uber, would you still have insured him? Again most insurers would say Yes

If this was the case, then the FOS would say: “So what is the problem then? You would have insured him, so you can’t now cancel”.It is worth noting here, that the FOS does not look at what is legal or not; they look at what is fair and right. Therefore they would say the policyholder did what he thought was right and acted in ‘Good Faith’ by disclosing all that was asked of him.Pursuing Uber for claims payouts

As we have just explained, going against individual drivers would be a very costly and lengthy approach, and unlikely to be successful for the insurer. They may instead consider actions against Uber or TfL, who allowed the situation to happen.However, as the contract of insurance is between the insurer and the driver, and does not involve Uber or the Regulator, this once again could lead to extremely expensive, long and complex judicial proceedings.To summarise, an insurer can go through the process, but it is very unlikely that they would successfully cancel the policy. Going against individual drivers wouldn’t seem to be cost-effective. Actions may be taken against Uber themselves or the regulators, but this could also lead to very complex judicial proceedings, which is an area of knowledge that goes beyond our area of expertise as an insurance broker.

No comments:

Post a Comment